FACT CHECKED

FACT CHECKED

Gone are the days when online banking solutions were considered as just useful “add-ons” offered along with physical banking services. Now, digital banking has become the norm. Data shows that the number of online banking users has skyrocketed over the past few years due to the digital adoption approach the world has taken.

Especially, the pandemic seems to have accelerated the need for online banking needs. People are willing to change banks if the alternative offers better apps and websites to operate their accounts. Data shows that the working-age population, especially the younger workers, prefer banks that offer better tools to access their money online.

However, the banks are not able to build digital adoption solutions themselves. Most rely on third parties to fulfill their digital needs. This has a serious impact on their ability to keep customers’ data secure. For most financial institutions, ensuring cyber security has become a major headache. As the number of online bank frauds continues to increase across the globe, the dark underbelly of digital payments is rearing its ugly head.

Ten charts that show the digital penetration and its side-effects in the banking industry:

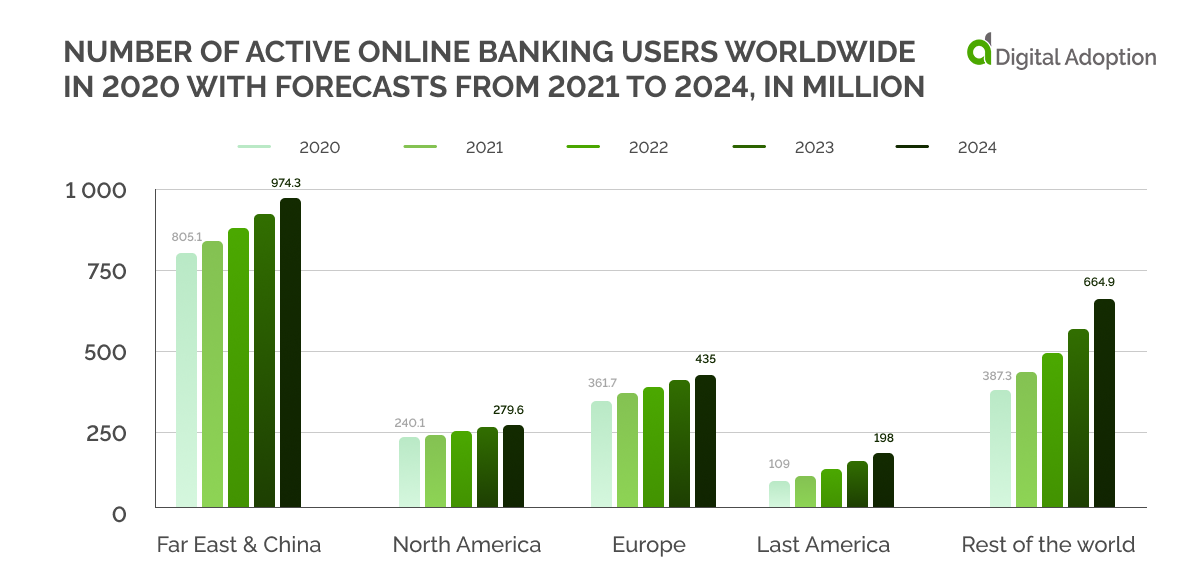

Number of active online banking users worldwide in 2020 & 2024 forecasts

Chart 1 shows the number of active online banking users worldwide and forecasts. Across all regions, the number of online banking users has multiplied by varying degrees. The sharpest growth was recorded in China and the Far East. Europe too witnessed a significant surge in such users.

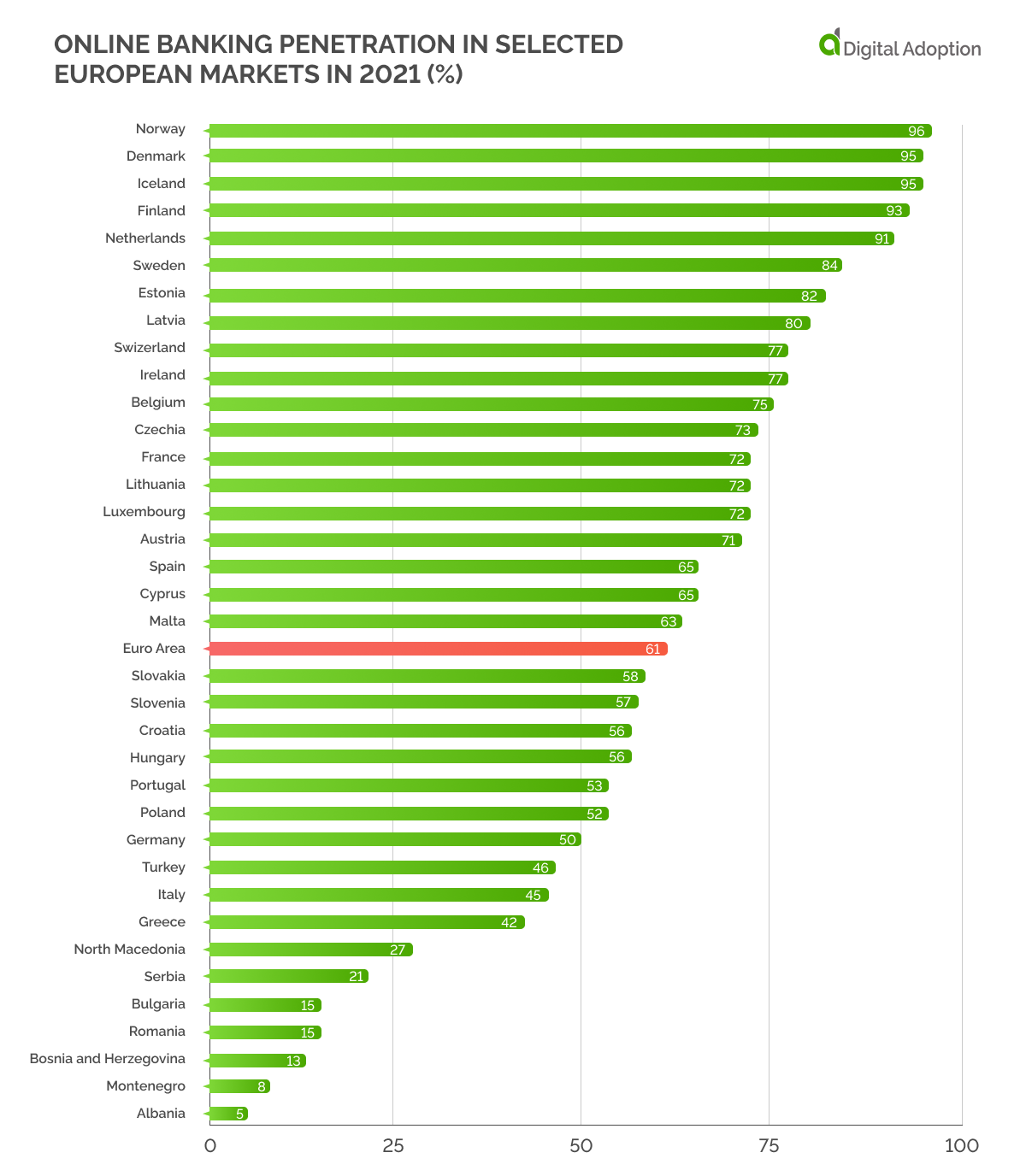

Online banking penetration in selected European markets in 2021

Chart 2 shows the share of people who use online banking in select European nations. In at least 27 countries, more than half the population uses online banking. And in eleven of them more than 75% use the digital adoption solution. Put together close to 60% users in the Euro area are familiar with online banking.

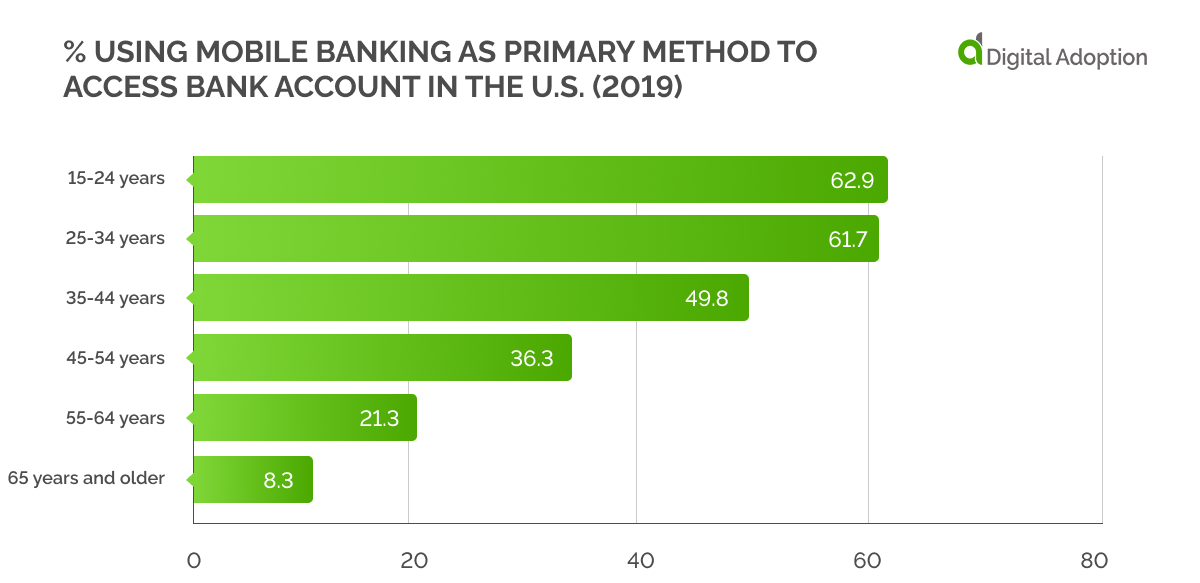

Number of people who are using mobile banking as primary method in the US

Chart 3 shows the share of the U.S. population across age groups which uses their mobile phone primarily to access their bank accounts. As can be observed from the chart, more than 60% of youngsters aged between 15 and 34 now access their accounts using mobiles. The share is nearly 50% even in the 35-44 age group. These numbers show that about half the working-age population are now into mobile banking.

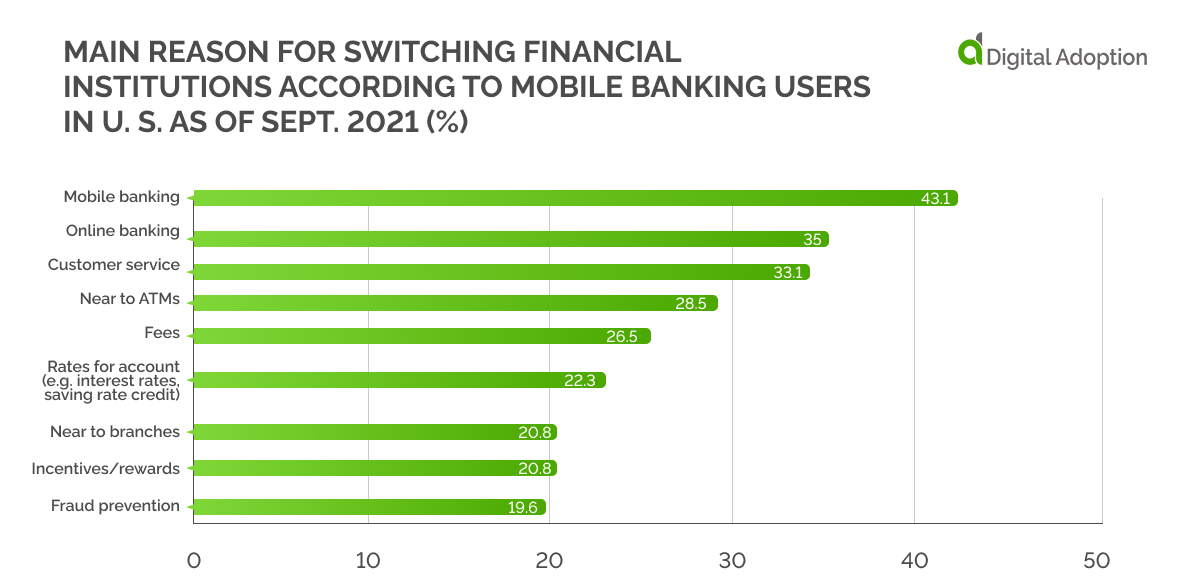

Main reasons people are switching financial institutions according to mobile banking users in the US 2021

Chart 4 shows the main reasons for customers in the United States to switch banks as of September 2021. More than 40% of customers said that mobile banking was the reason for the switch, followed by 35% who changed their banks for online banking. So the top two reasons for changing financial institutions were related to digital banking solutions.

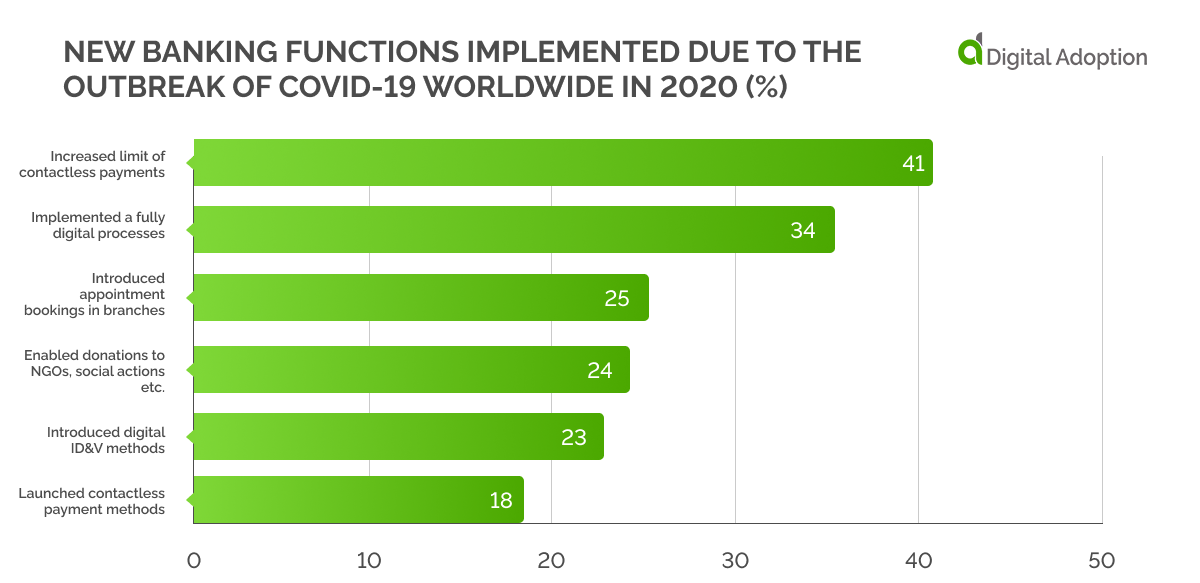

New banking functions implemented due to the outbreak of Covid-19 worldwide

Chart 5 shows the new banking functions implemented worldwide due to the pandemic. Due to the movement restrictions during the pandemic, neither the banks nor the customers were able to do physical transactions. This prompted the banks to go digital. About 40% of them increased their limit of contactless payments and 34% implemented a fully digital process.

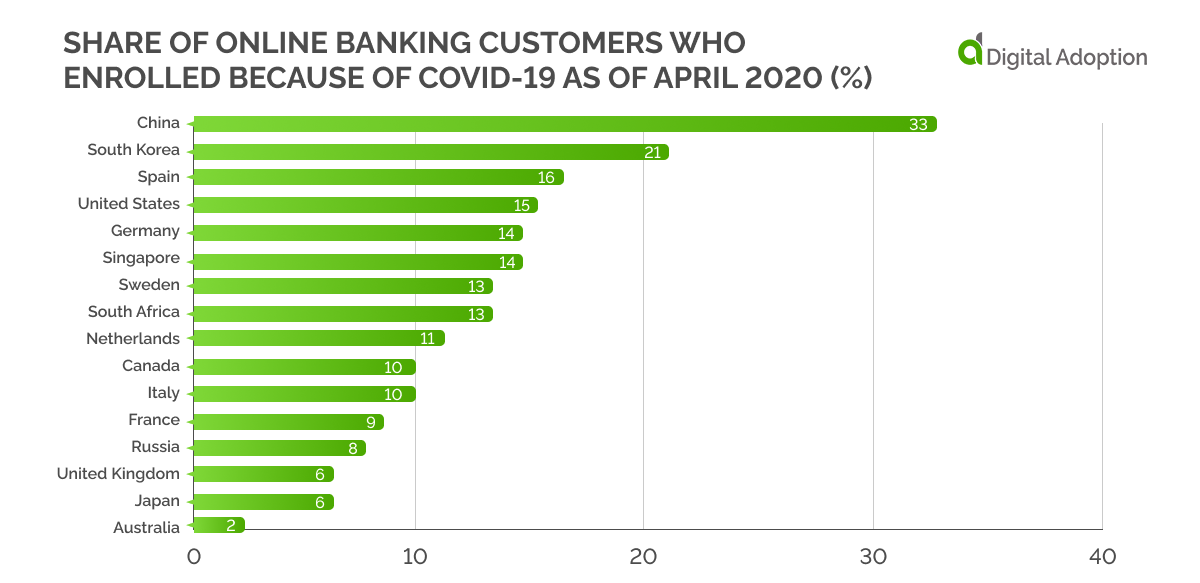

Share of online banking customers who enrolled because of Covid-19

Chart 6 shows that a fresh wave of customers enrolled for online banking due to the movement restrictions during the pandemic. Especially in China, where a zero-covid policy was enforced by the government with severe and sudden lockdowns in urban clusters, 33% of the bank customers enrolled for digital banking due to the pandemic. A similar increase in online customers was also observed in South Korea, Spain, and the United States.

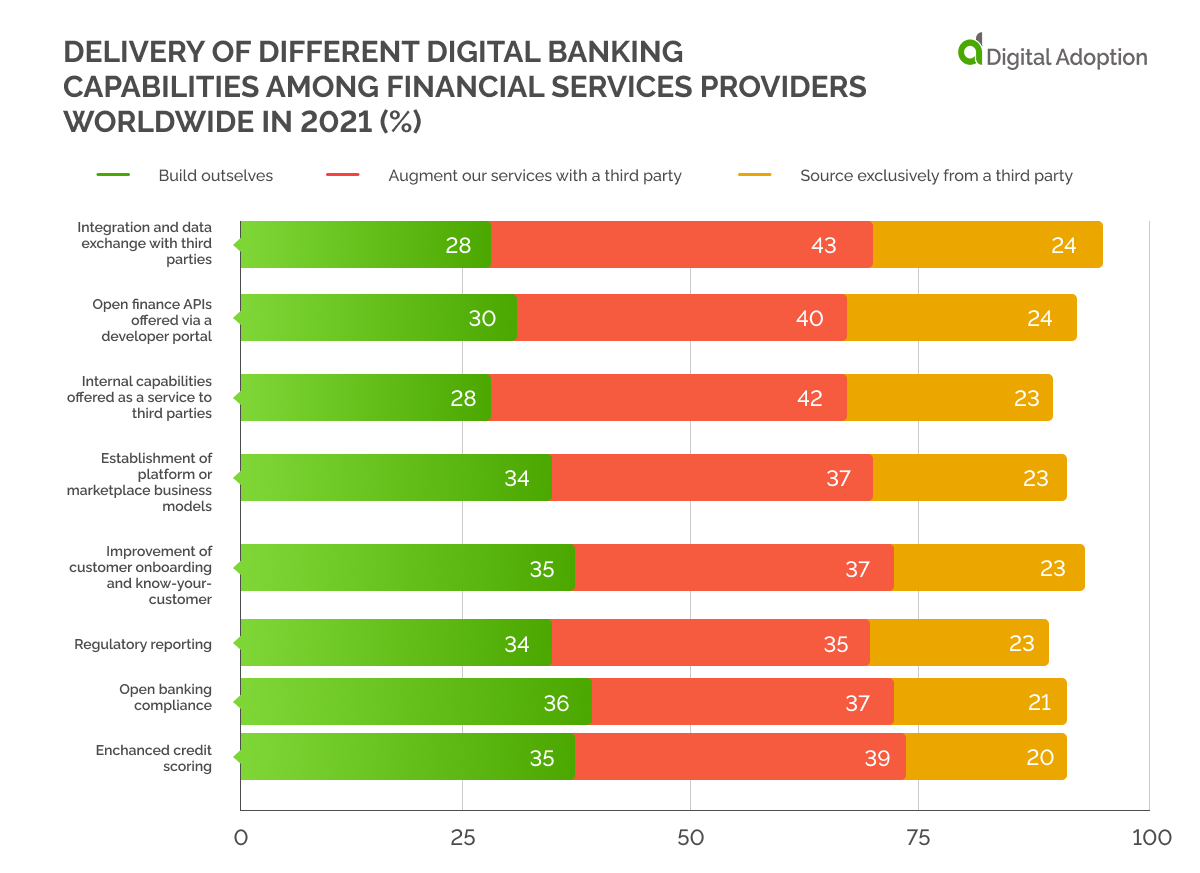

Delivery of different digital banking capabilities among financial service providers worldwide in 2021

Chart 7 shows the delivery of different digital banking capabilities among banks in 2021. Banks rely on third parties to build their digital solutions but do not rely solely on them. As can be observed from the graph, for most digital solutions, banks augment their services with a third party, and only a smaller share of banks either builds the solutions themselves or source them from a third party exclusively.

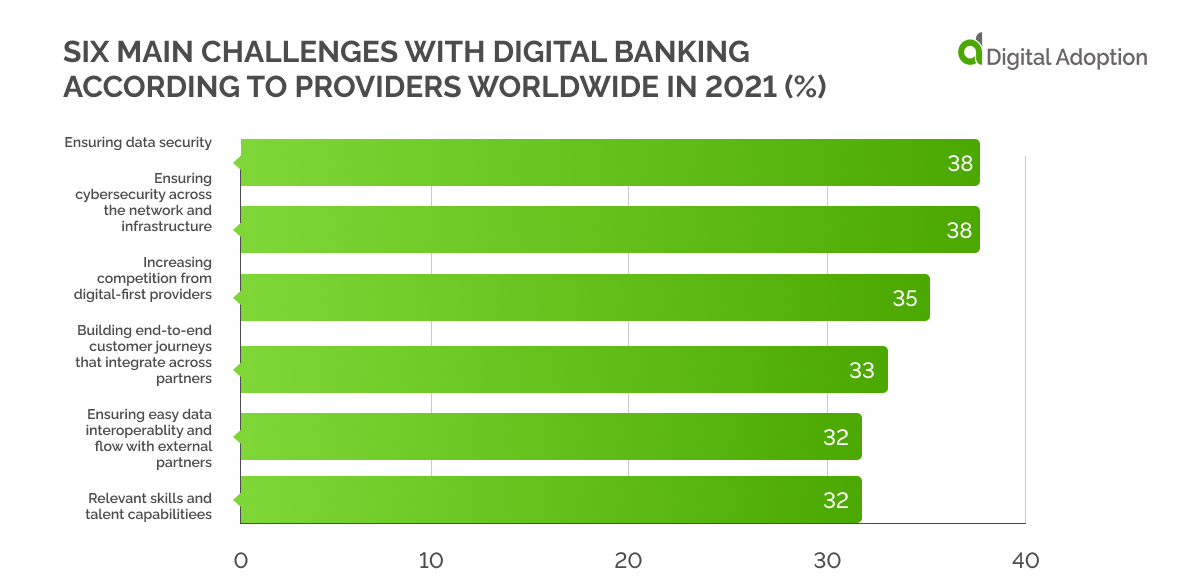

Six main challenges with digital banking according to providers worldwide 2021

Chart 8 shows the main challenges in digital banking. Of course, with the advent of digital banking, the biggest drawback is ensuring the security of their customers. About 40% of banks felt that ensuring data security and ensuring cybersecurity across their network were the top two challenges they face.

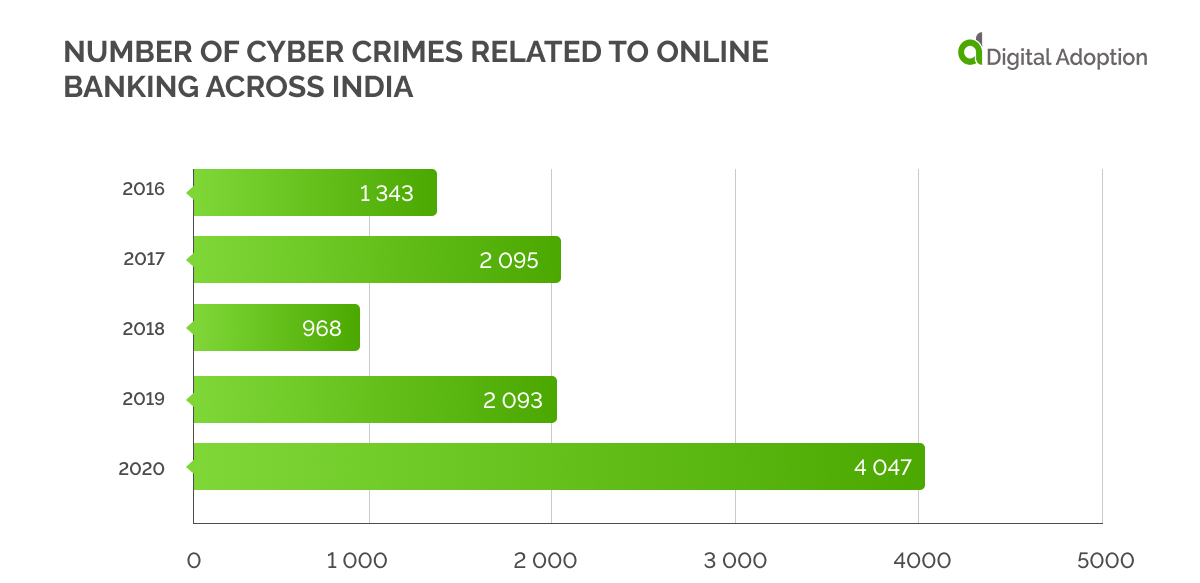

Charts 9 and 10 show the value and the number of banking frauds in the U.K. and India, respectively. The numbers have been on an increasing trend in both countries. A trend that underlines the dark underbelly of the online banking system with cyber frauds managing to swindle hard-earned money using various online tools.

Value of annual online banking fraud losses in the UK (GBP)

Number of cyber crimes related to online banking across India